La presentación PowerPoint de la presentación en ESEADE de «Monetary Equilibrium and Nominal Income Targeting» (Routledge).

Archivo de la etiqueta: NGDP targeting

Presentación: Monetary Equilibrium and Nominal Income Targeting

Imagen

Monetary Equilibrium and Monetary Theory: The Case of Nominal Income Targeting, by Nicolas Cachanosky (Routledge International Studies in Money and Banking) 1st Edition

This book examines the case of nominal income targeting as a monetary policy rule. In recent years the most well-known nominal income targeting rule has been NGDP (level) Targeting, associated with a group of economists referred to as market monetarists (Scott Sumner, David Beckworth, and Lars Christensen among others).

Nominal income targeting, though not new in monetary theory, was relegated in economic theory following the Keynesian revolution, up until the financial crisis of 2008, when it began to receive renewed attention. This book fills a gap in the literature available to researchers, academics, and policy makers on the benefits of nominal income targeting against alternative monetary rules.

It starts with the theoretical foundations of monetary equilibrium. With this foundation laid, it then deals with nominal income targeting as a monetary policy rule. What are the differences between NGDP Targeting and Hayek’s rule? How do these rules stand up against other monetary rules like inflation targeting, the Taylor rule, or Friedman’s k-percent?

Nominal income targeting is a rule, which is better equipped to avoid monetary disequilibrium when there is no inflation. Therefore, a book that explores the theoretical foundation of nominal income targeting, comparing it with other monetary rules, using the 2008 crisis to assess it and laying out monetary policy reforms towards a nominal income targeting rule will be timely and of interest to both academics and policy makers.

TABLE OF CONTENTS

1. Introduction

2. Free Banking and Monetary Equilibrium

3. The Productivity Norm and Nominal Income Targeting

4. Nominal Income Targeting and Monetary Rules

5. Nominal Income Targeting with Monetary Disequlibrium

6. Nominal Income Targeting as Policy Outcome versus Market Outcome

7. NGDP Targeting and the 2008 crisis

8. Policy Reforms Towards Nominal Income Targeting as a Rule

ABOUT THE AUTHOR

Dr Nicolas Cachanosky is an Assistant Professor of Economics at Metropolitan State University of Denver, Department of Economics.

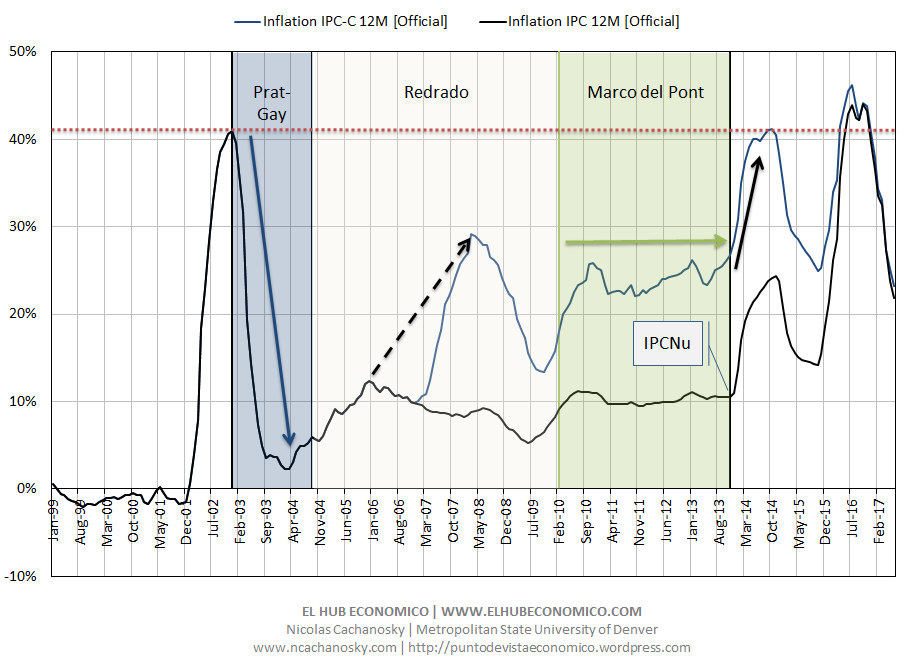

Inflación en Argentina

En el día de ayer se publicaron los datos oficiales de inflación del mes de junio, completando así el panorama inflación a mitad de año. A continuación tres gráficos de inflación. Luego unos breves comentarios.

Entrevista con Reinvent Money

Entrevista, en inglés, con la gente de Reinvent Money. Hablamos de diversos temas relacionados a teoría monetaria. Desde problemas monetarios en Argentina a casos históricos de banca libre, pasando por el Bitcoin y también sobre la política de la Reserva Federal luego de la crisis del 2008.

SMP: Should Central Banks Target NGDP?

El último fin de semana de Abril tuvo lugar en el Center for Free Enterprise en West Virginia University una conferencia sobre si los bancos centrales deben tener metas de ingreso nominal.

En este post del SMP resumo la conferencia y algunas de las presentaciones.

That was the topic of a conference organized by the Center for Free Enterprise at West Virginia University that took place on Saturday, April 25. The conference was divided in two sessions: one where theoretical aspects of NGDP were discussed and another that took a more empirical approach to the matter. I presented in the second session on how to spot if NGDP targeting is, in fact, too loose.

Besides the presence of Scott Sumner, probably the best known proponent of NGDP targeting, other presenters included Thomas Hogan, Alexander W. Salter, Ryan Murphy, Joshua Hendrickson, Robert Lester, and Vipin Veetil. While all papers endorsed NGDP targeting in one way or another, at least as a superior norm to other principles such as price stability or the Taylor rule (Hendrickson and Lester), the papers also focused on either if this holds under a free banking system (Salter) or if the rule could put the economy in an inferior equilibrium (Hogan). Even though I found all presentations interesting, I’ll briefly comment on just two of them.

Center for Free Enterprise: Should Central Banks Target NGDP

El Center for Free Enterprise, dirigido por Andy Young, en West Virginia University organizó una conferencia sobre si los bancos centrales deben estabilizar el ingreso nominal. Scott Sumner, posiblemente el defensor más conocido de esta postura estuvo presente.

Incluyendo el paper de Sumner, se presentaron y discutieron un total de 8 papers sobre el tema. La conferencia fue muy interesante, con papers de todos los estilos. Entre otros, estuvieron presente Thomas Hogan, Alex Salter, Josh Hendrickson, Richard Wagner y Ryan Murphy.

En mi caso presenté un borrador donde sugiero qué variables observar para definir si el PBI nominal esta siendo «too loose for too long.» En mi paper sugiero que el 5% de crecimiento entre el 2002 y el 2008 fue, de hecho, excesivo. Si bien esto sólo no explica la profundidad y extensión de la crisis subprime sí contribuye a explicar la burbuja inmobiliaria.

Aquí la presentación del paper en la conferencia.

NGDP Targeting y la Tasa Natural de Interés

Dos importantes posturas de política económica ofrecen resultados opuestos. Por un lado, el NGDP Targeting del Market Monetarism que sostiene que un crecimiento del 5% del PBI nominal en Estados Unidos antes de la crisis supbrime era una política adecuada. Por el otro, la Regla de Taylor que sostiene que la Reserva Federal fue demasiado expansiva por demasiado tiempo (al menos entre el 2002 y el 2004/05).

En un post anterior discutía cómo otras variables, como el precio de bienes intermedios o la serie de Gross Output, podían de hecho sugerir que el crecimiento al 5% del PBI nominal de hecho fue excesivo, tal cual sugiere la Regla de Taylor.

En esta ocasión expando las mismas conclusiones con dos gráficos. El primero muestra la tasa natural para Estados Unidos según los cálculos actualizados de Laubach and Williams (2003). El segundo gráfico muestra una Regla de Taylor «ajustada», donde en lugar de asumir una tasa de interés real del 2.5% más la inflación del último año, la regla corrige desvíos en torno a la tasa natural de interés de Laubach and Williams.

Los dos gráficos sugieren que la política monetaria de la Fed empujó la tasa de interés por debajo de su nivel de equilibrio de «largo plazo». El segundo gráfico también muestra que si se toman las estimaciones de Laubach y Williams como válidas, entonces la regla de Taylor se encuentra significativamente por encima de lo que sería un valor de equilibrio.

Los dos gráficos sugieren que la política monetaria de la Fed empujó la tasa de interés por debajo de su nivel de equilibrio de «largo plazo». El segundo gráfico también muestra que si se toman las estimaciones de Laubach y Williams como válidas, entonces la regla de Taylor se encuentra significativamente por encima de lo que sería un valor de equilibrio.

Aquí el paper actualizado.

¿Qué regla monetaria deberían aplicar los bancos centrales?

El debate tradicional de la política monetaria que debería aplicar la Fed o cualquier Banco Central divide a los economistas entre las reglas y la discrecionalidad (en este foro sabemos, además, que Hayek encabeza una lista de economistas que propusieron otras alternativas). Pero si nos circunscribimos estrictamente al debate tradicional, quienes creemos en las reglas también nos encontramos divididos en diferentes alternativas:1. Inflation targeting, 2. Regla de Taylor, 3. Regla de Friedman, 4. NGDP targeting, 5. Norma de la productividad, 6 Regla de la tasa de interés natural, son algunas de ellas.

Nicolás Cachanosky cuestionó recientemente al NGDP targeting. Junto a Erwin Rosen, nosotros definimos la NRI Rule.

John Cochran referenció estos trabajos en su nueva columna en el Mises Daily, donde además cita a Alexander William Salter, “Is There a Self-Enforcing Monetary Constitution?”, y el trabajo de Alexander William Salter y Thomas Hogan, “A Hiccup in NGDP Targeting: Supply-Side Problems with Demand-Side Policy.” El mismo Cochran nos proporciona de una evaluación de las reformas monetarias planteadas desde la Escuela Austriaca.

Tomamos aquí un extracto:

In a recent Quarterly Journal of Austrian Economics article, “The Natural Rate of Interest,” Edwin Rosen and Adrian Ravier explain why. Central banks are likely to be key institutions for the “foreseeable future.” Hence, the end of “government interference with the market in general and its manipulation of the money supply in particular” is “an unrealistic aspiration.” Given this realty, the “objective becomes how best to minimize its [central banking’s] unfortunate negative impact on the economy.” Austrians are uniquely positioned to provide answers that are more likely to ensure suggested rules that address the “two significant weaknesses” all central banks face: “susceptibility to political pressure and inadequate economic knowledge.” Moreover, Austrians best understand the true nature of “sound money” and its “symptoms … full employment and economic stability.” Rosen and Ravier recommend a rule “that follows Wicksell’s monetary equilibrium doctrine.” While they recognize the rule would “not eliminate short term price fluctuations” they believe their proposed rule would lead to results more conducive to “inflation free economic stability” and “sustained growth” which has been missing in the US since the inception of the Fed. Other Austrian or Austrian-influenced economists have already made significant contributions to the discussion. Examples include Nicolás Cachanosky, “NGDP Targeting: Is 5 Percent Too Much?” Alexander William Salter, “Is There a Self-Enforcing Monetary Constitution?” and Alexander William Salter and Thomas Hogan, “A Hiccup in NGDP Targeting: Supply-Side Problems with Demand-Side Policy.” Cochran provides an assessment of some proposed reforms from an Austrian perspective.

WP: NGDP Targeting: Is 5 Percent Too Much

This is the title of my latest draft (of which I very much welcome comments) about Market Monetarist’s NGDP Targeting.

Since I don’t want the title to send the wrong impression, I want to clarify is that I don’t question the NGDP Targeting principle. The topic of the paper is whether or not there are signs that a 5% growth of NGDP before the subprime crisis wasn’t in fact too much.

There is some tension. On one side Taylor Rule and the productivity norm suggest that monetary policy was too loose during the ca 2002-2007 period. But Market Monetarism does not support this reading. The problem was the fall of NGDP in 2008, not that NGDP was growing to fast. This also requires to deal with the question of how a housing bubble took place without an excess of money supply.